Is My Retirement On Track?

Planning for retirement can feel overwhelming, especially if you’ve been working and saving for decades and still wonder, Is my retirement on track? In this article, we’ll walk through a clear process to help you evaluate your retirement readiness, estimate how much money you’ll need, and assess whether you can retire early.

Start With a Detailed Retirement Budget

The first question to ask is, “Is my retirement on track?” The best way to begin answering that is to prepare a budget. And yes, I know what some of you might be thinking—budgets aren’t fun. Maybe you’ve tried them in the past, or you’ve avoided them altogether. But going into retirement, having a budget is essential—no matter how much money you have.

Once you stop earning a paycheck and begin drawing from your portfolio, you need to know how much to withdraw each year—and whether your investments can support that. We use budget worksheets in our Retirement Launchpad guide to help break expenses down into categories, including:

- Housing expenses: Will you keep your current home, downsize, or buy a second property? Break down property taxes, maintenance, and mortgage expenses separately for each.

- Transportation: Include costs for every car, RV, or boat you own or plan to own in retirement.

- Lifestyle spending: This includes dining, entertainment, travel, and expenses related to adult children.

Comparing your current spending to expected retirement spending helps bridge the gap between your current income and the income you’ll need to draw from your savings and investments.

Determine What You’ll Need at Full Retirement Age

Next, figure out how much money you’ll need at full retirement age, which is 67 for most people. That’s when you become eligible for unreduced Social Security benefits. For this example, let’s say you and your spouse plan to live on $120,000 per year in retirement.

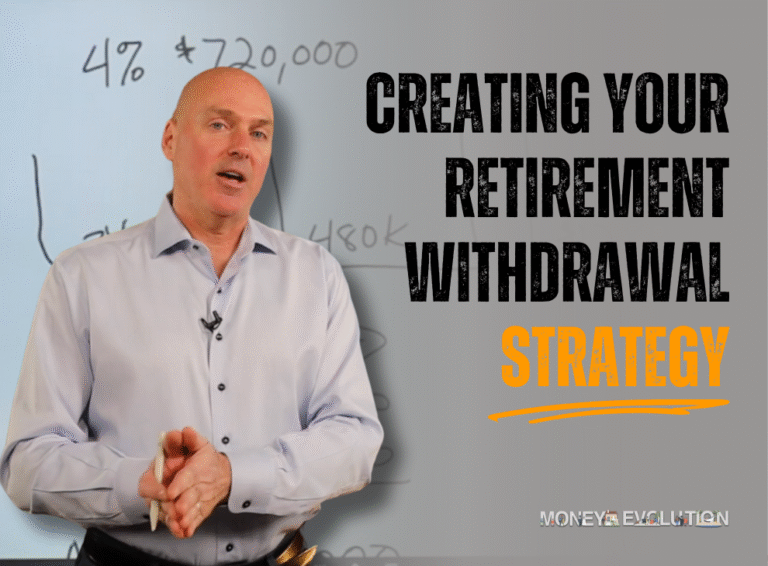

If Social Security provides $60,000, then you’ll need to withdraw $60,000 per year from your retirement accounts. Using the 4% rule, you’d divide $60,000 by 0.04, which equals $1.5 million needed in your portfolio.

This simple math doesn’t factor in inflation or taxes, but it’s a helpful starting point. If you already have that amount saved—or will by age 67—you may be in great shape. At this point, you’re closer to answering, is my retirement on track?

Can I Retire Early and Still Stay on Track for Retirement?

Retiring before age 67 is a dream for many people. But doing so requires careful planning. Let’s assume both spouses want to retire at 60 and still spend $120,000 per year. If they delay Social Security and don’t have pensions, they’ll need to fund the full amount from their investments.

That’s $120,000 × 7 = $840,000 needed for the early years alone.

Add that to the $1.5 million required for later retirement, and you get a total of $2.34 million needed to retire at 60 under these assumptions.

The Bucket Strategy for Early Retirement Planning

To make this strategy work, we often use a bucket approach. In this example:

- Bucket #1: $240,000 in very safe, liquid assets like money markets or short-term CDs. This covers the first two years of expenses.

- Bucket #2: $600,000 invested a bit more aggressively to cover the following five years.

- Growth Bucket: Any remaining assets can go here and be invested for long-term growth.

By splitting your portfolio this way, you avoid selling growth assets during a downturn. If the market drops, you draw from the safer buckets while giving your growth assets time to recover. This helps reduce the risk of drawing down your portfolio too quickly during a bad market year.

Additional Income Strategies to Stay on Track

If you’re wondering, is my retirement on track and the math isn’t working out, consider generating additional income to reduce portfolio withdrawals:

- Dividend portfolios: Provide consistent income without selling shares.

- Annuities: Offer guaranteed lifetime income, though they require careful evaluation.

- Fixed income accounts: Create predictable interest payments to reduce reliance on your investment portfolio.

The more income you can generate, the less pressure you put on your investments to produce the full $60,000 or $120,000 per year.

Three Part Framework – Is My Retirement On Track?

Here’s the three-part framework:

- Build a realistic retirement budget

- Calculate what you’ll need at full retirement age

- Plan for early retirement using a bucket strategy

Start putting the pieces together today so you can retire with purpose, confidence, and a clear understanding of what it takes to stay on track.