Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

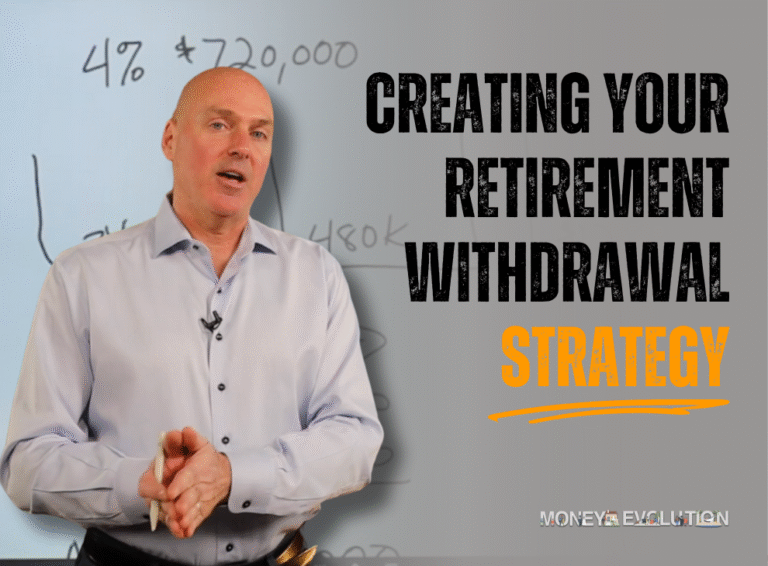

The impact of a flat market on retirement can be more damaging than most people realize. Even if you’re following a solid withdrawal strategy, a prolonged period of little to no market growth can chip away at your savings faster than expected. In this article, we’ll walk through a hypothetical retirement scenario to show how sideways markets affect your income—and what you can do to protect your plan.

I recently talked about how to create a bucket strategy to generate $120,000 a year of retirement income. In that article, I went through how the bucket strategy works and some of the risks that come along with it. In this article, I want to go a little deeper into what actually happens when we go through a flat or sideways market—and how you should think about operating those buckets.

Let’s walk through a hypothetical situation. Again, this is just hypothetical—your situation could be very different. Let’s say someone wants to get $80,000 a year from their retirement portfolio, and they have $2 million of total portfolio assets. Right away, you might already be doing the math in your head: $80,000 out of a $2 million portfolio is exactly 4%.

That’s what we commonly refer to as the 4% rule—a general rule of thumb that we often use. It’s not a guarantee, of course, but there’s been a lot of research done on this. The basic idea is that if you limit your withdrawals to 4% or less, you have an above-average chance that your money will last the rest of your life.

Now, when that research was originally done back in the early 1990s, it was based on a 20-year retirement period. Success was defined as still having at least $1 in the portfolio after 20 years.

But depending on your age and longevity, 20 years might not be enough. I have a grandfather who’s about to turn 97, and I think he retired in 1986. Hopefully, you’ll have that kind of longevity too.

When you’re planning out your buckets, it’s easy to overlook the impact of a flat market on retirement because it doesn’t feel as dramatic as a crash—but it can be just as dangerous over time. Let’s break this down using a three-bucket strategy for income planning.

Before we get into the exact bucket allocations, here’s an important concept: If you were to invest this money into a conservative short-term vehicle that earns about 4% interest—something realistic as of 2025—you wouldn’t actually need the full $560,000 to fund seven years of $80,000 withdrawals. Thanks to interest earnings (assuming 4%), you’d only need about $480,000. That’s the number we’ll use for this example.

Annual withdrawal need: $80,000

We’re going to keep things simple here and leave inflation and taxes out of it, just like I usually do when illustrating things on the whiteboard. Those things make the math more complicated. That’s where having planning software really helps—being able to calculate taxes, inflation, portfolio growth, and gaps over time.

But for this example, we’re just going to assume you need $80,000 a year for the rest of your life. Most people’s situations are more complex—you might have one spouse retiring earlier, Social Security kicking in at different times, maybe a mortgage payoff.

The idea behind the bucket strategy is that as long as the markets are going up—or at least not going backward—you can replenish Bucket #2 from your growth bucket (Bucket #3) each year. Then you refill Bucket #1 from Bucket #2.

That way, you’re always maintaining seven years of retirement income in Buckets #1 and #2.

But the big question is: what happens when the market goes down? Or more accurately—when the market goes down—because it will. That’s just a fact based on over 100 years of stock market history.

Sometimes the market bounces back quickly, like in 2018, 2020 with COVID, or even 2022. But those fast recoveries aren’t always the norm.

If we go back to the dot-com bubble, the market peaked in 2000 and took three years to reach the bottom around late 2002. It bounced a little, then dropped again in 2003.

Eventually, the market recovered—but slowly. By around 2007 or 2008, we were back at the same level as in 2000. Then the Great Financial Crisis hit, and we dropped even more—about 57%.

Let’s say your growth bucket starts with $1,520,000. If the market struggles, you may have to let Buckets #1 and #2 drift down, taking $80,000 a year out of them while hoping the market recovers.

Hopefully, within seven years—when Buckets #1 and #2 are depleted—your growth bucket has recovered to $1,520,000 or higher. At that point, you’d want to refill those buckets by taking out another $480,000.

That would leave you with $1,040,000 in your growth bucket.

Now, if you’re still taking out $80,000 a year, you’re essentially withdrawing approximately 8% from that growth bucket.

Unless you’re earning at least 8% per year, that growth bucket will continue to shrink—especially since you’re still using it to fund Buckets #1 and #2.

That’s how just one flat or sideways market can put you in a position where your withdrawals aren’t 4% anymore.

Look at Your Expenses

One of the things you should do is take a close look at your expenses. What are the things you absolutely have to have—your basic needs like housing, food, transportation, insurance? And what are some of the more discretionary expenses like travel or entertainment?

I get it—you’ve worked your whole life, saved your money, and now you want to enjoy your retirement. But if the market is going sideways, you may want to consider trimming back some discretionary spending temporarily. That could help buy you a couple more years for your portfolio to recover.

Add Predictable Income Sources

In the previous article, we talked about adding more predictable income. Some examples include:

Predictable income streams help soften the impact of a flat market on retirement, giving you more flexibility to delay withdrawals or reduce portfolio pressure.

I hope that makes sense a little bit—how to set this up, how to manage it, and what to be aware of. These hypothetical illustrations are meant to simplify the concepts so you can think about how they might apply to your own situation.

But in reality, there’s a lot of variability—different income sources, changing expenses, timing strategies. That’s where a real financial plan makes a big difference.

We use some great software that calculates taxes, models retirement cash flow, and takes all those moving parts into account.